First they ignore you. Then they ridicule you. And then they attack you and want to burn you.

Nicholas Klein (1914)

David Gerard, the author of Attack of the Fifty Foot Blockchain (2017), declares that if “you were silly enough to put personal data into an append-only ledger which is a proof-of-work blockchain — that’d be flat-out insane.” Numerous other authors discount blockchain, including one of my favorites, David Gabler. I regularly post on blockchain topics to present different contexts and have never advocated a single approach, like blockchain, as a solution for all problems. Some authors create straw-man arguments against blockchain and others offer decision models to help decide whether or not to use blockchain. The blockchain space continues to evolve and if you are researching, you should check the vintage of the articles. Many were written between 2017 and 2019, right before a vendor shakeout occurred in late 2020.

This is a good time to examine the regulatory treatment of blockchain, specifically from California’s CCPA, the EU’s GDPR and France’s Data Protection Authority (CNIL). Each of these regulators started from the same philosophical point as blockchain; consumers should have control of their data. CNIL provides good advice to follow because they have the power to investigate and issue sanctions. They advise that you should not put personal data into an append-only ledger. I agree that it would be insane to put social security numbers into any system, not just blockchain.

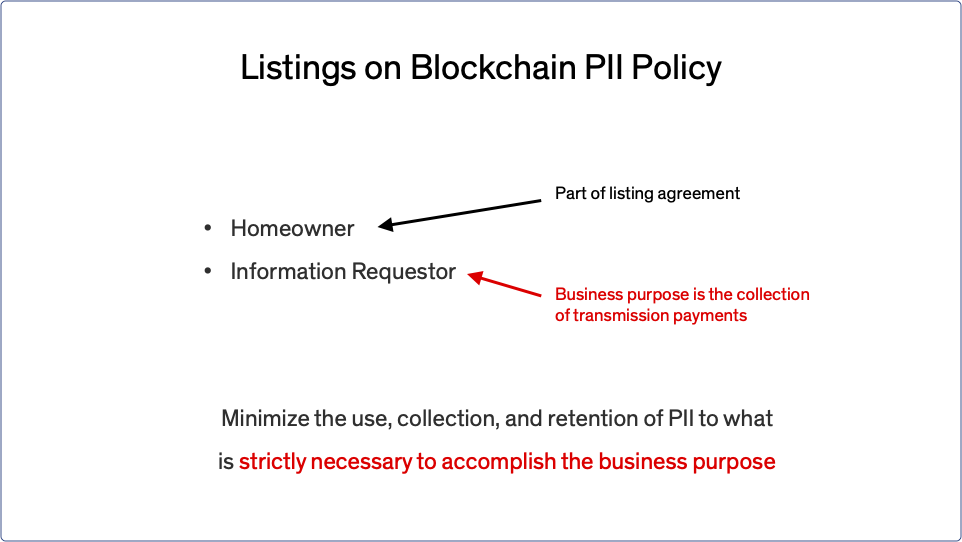

The purpose of residential real estate sales is not to sell Personally Identifiable Information (PII) about homeowners. Collecting and/or selling consumer shopping information includes the handling of PII and would be the kind of activity that regulators are concerned about. If blockchain was used to distribute consumer behavior information, consumer requests to delete their information would not be possible.

When the blockchain recovers transmission fees for the listing, it is necessary to document the receipt of payment. Collecting payment information is not the same business purpose as collecting and/or selling consumer shopping behaviors.

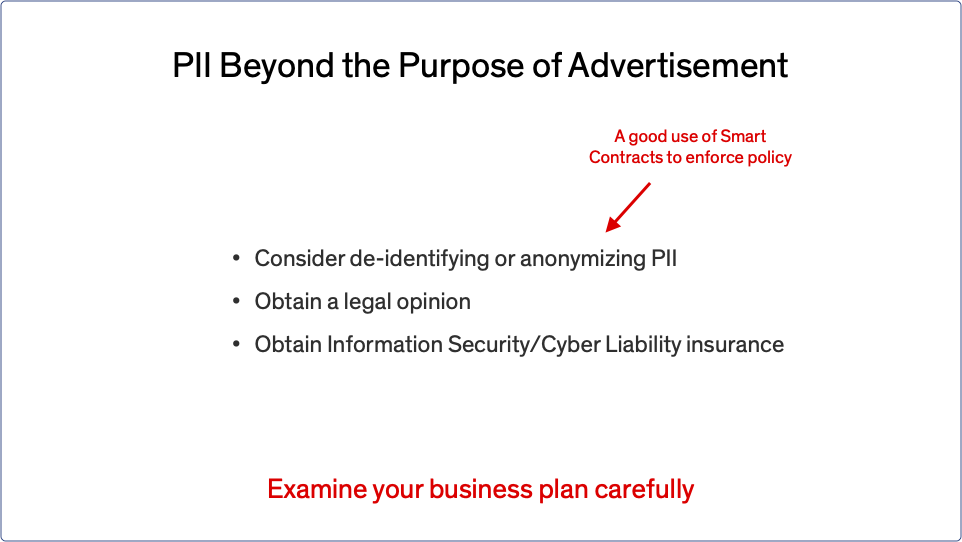

If your business is going to extend beyond the advertising of listings and cooperating with others to provide detailed information, then you should proceed cautiously. Remember that once written, it is impossible to delete information from most blockchains. I say most because it is possible to share ledgers that are not the append-only variety but this is a deeper conversation so I will leave you with traditional cautions about distributing consumer shopping patterns; talk to a lawyer and make sure you are covered by insurance.

Leave a Reply